Every year, american businesses face the challenge of preparing corporate tax returns, a task that carries major financial and legal weight. Nearly one in four small business owners admit to making at least one mistake when filing, which can lead to costly penalties. Understanding what a corporate tax return involves helps companies avoid these pitfalls, maintain compliance, and make smarter decisions about their business finances.

Defining Corporate Tax Returns and Purpose

Corporate tax returns represent a critical financial document that businesses use to report their annual income, expenses, and calculate their tax liability to federal and state governments. Congress defines corporate income tax as a systematic approach to taxing business profits, calculated by subtracting total associated costs from gross income.

The primary purpose of corporate tax returns extends beyond mere financial reporting. These documents serve multiple essential functions for businesses and government agencies:

- Determining precise tax obligations

- Documenting business financial performance

- Ensuring legal compliance with tax regulations

- Providing a transparent record of corporate financial activities

According to the Tax Foundation, corporations must file these returns to report comprehensive income details and calculate taxes owed. This process involves meticulously recording all business revenue streams, claiming permissible deductions, and applying relevant tax credits. Small businesses, in particular, must understand that corporate tax returns are not just administrative tasks but strategic financial documents that can significantly impact their fiscal health.

Navigating corporate tax returns requires careful attention to detail and a thorough understanding of current tax laws. For small businesses seeking comprehensive guidance, our guide to filing business taxes offers in-depth insights into managing this critical financial responsibility effectively.

Types of Business Entities Filing Returns

The Internal Revenue Service identifies several key business structures that have distinct tax filing requirements. Understanding these different entity types is crucial for small business owners to ensure proper tax compliance and optimize their financial strategies.

The primary business entities that must file tax returns include:

- Sole Proprietorships: Individual-owned businesses reporting income on personal tax returns

- Partnerships: Business structures where income passes directly to individual partners

- Corporations: Separate legal entities with more complex tax reporting

- S Corporations: Special corporate structures with unique tax treatment

- Limited Liability Companies (LLCs): Flexible business structures with varied tax options

According to the Tax Policy Center, many small businesses are considered pass-through entities. These businesses, including sole proprietorships, partnerships, LLCs, and S corporations, have a unique tax characteristic: business income passes directly to owners, who then report this income on their individual tax returns. This approach allows these businesses to avoid corporate income tax, potentially providing significant tax advantages.

Small business owners navigating these complex filing requirements can benefit from specialized guidance. Our essential guide to small business tax filing provides comprehensive insights into selecting the right business structure and understanding its specific tax implications.

Key IRS Filing Requirements and Deadlines

The Internal Revenue Service establishes specific tax filing requirements and deadlines that vary depending on the type of business entity. Understanding these crucial timelines is essential for avoiding penalties and maintaining good standing with tax authorities.

Key tax filing deadlines for different business structures include:

- Corporations: Form 1120 due April 15

- Partnerships: Form 1065 due March 15

- S Corporations: Form 1120S due March 15

- Sole Proprietorships: Schedule C with personal tax return due April 15

- LLCs: Deadline depends on tax classification (partnership or corporation)

Modern tax compliance has been significantly simplified by electronic filing options. The IRS now offers electronic filing for various business tax forms, including employment tax returns, information returns, partnership returns, corporate returns, and returns for estates, trusts, and exempt organizations. This digital approach streamlines the filing process, reduces errors, and provides faster processing times.

To ensure you never miss a critical tax deadline, consider reviewing our comprehensive tax deadline guide. Proactive planning and understanding these key filing requirements can help small businesses maintain compliance and avoid costly penalties.

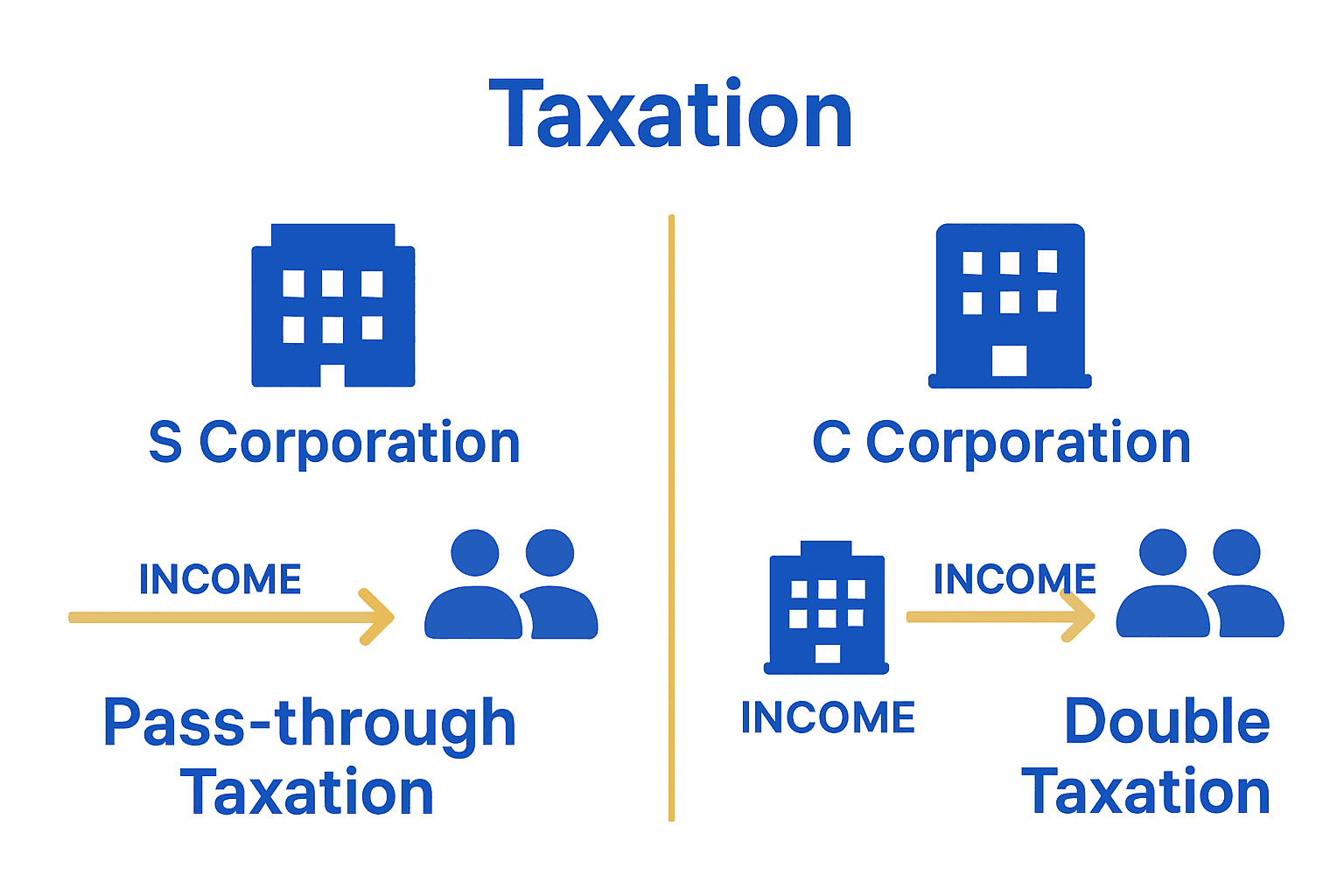

Understanding S Corporation vs. C Corporation Returns

The Internal Revenue Service distinguishes between S corporations and C corporations through their unique tax filing and reporting requirements. These two corporate structures represent fundamentally different approaches to business taxation, with significant implications for small business owners and their financial strategies.

Key differences between S and C corporations include:

- Tax Filing: C corporations file Form 1120, while S corporations file Form 1120-S

- Taxation Method: C corporations pay corporate-level taxes; S corporations have pass-through taxation

- Shareholder Limits: C corporations have unlimited shareholders; S corporations are limited to 100

- Shareholder Types: C corporations allow diverse shareholder types; S corporations have restrictions

- Profit Distribution: Different rules govern how profits can be distributed

According to New Jersey Treasury, the most critical distinction lies in taxation structure. C corporations are separate legal entities subject to corporate income tax, which can potentially result in double taxation – meaning the corporation pays taxes on profits, and shareholders pay taxes again on dividends. In contrast, S corporations pass income directly to shareholders, who report it on individual tax returns, effectively avoiding this double taxation scenario.

Small business owners exploring corporate structures can gain deeper insights by reviewing reasons to choose an S Corp, which can help determine the most advantageous approach for their specific business needs and financial goals.

Common Mistakes and Compliance Risks

Government Accountability Office research reveals that small businesses frequently encounter critical compliance challenges that can result in significant financial and legal consequences. Understanding these potential pitfalls is essential for maintaining good standing with tax authorities and avoiding costly penalties.

Common corporate tax return mistakes include:

- Incorrect Entity Classification: Misidentifying business structure

- Income Underreporting: Failing to accurately report all business revenue

- Employee Misclassification: Incorrectly categorizing workers as independent contractors

- Inadequate Record-Keeping: Poor documentation of financial transactions

- Improper Deduction Claims: Incorrectly applying business expense deductions

According to the Government Accountability Office, these errors can trigger serious consequences, including comprehensive tax audits, substantial financial penalties, and potential legal complications. Incorrect entity classification and improper deduction claims are particularly risky, as they can lead to immediate scrutiny from tax authorities and potentially result in significant financial repercussions.

To minimize these risks and ensure accurate tax reporting, small business owners should consider consulting a professional tax preparation service that can provide expert guidance and help navigate the complex landscape of corporate tax compliance.

Take Control of Your Corporate Tax Returns with Trusted Local Expertise

Filing corporate tax returns can feel overwhelming with all the specific IRS requirements, deadlines, and risks of costly mistakes that the article highlights. Small business owners often struggle with entity classification, correct deductions, and understanding the differences between S and C corporations. Avoid the stress and potential penalties by partnering with experienced tax professionals who know the local Akron Ohio landscape inside and out.

Get reliable support tailored to your business type and financial situation by visiting APC1040.com. Our dedicated team offers affordable, transparent tax preparation backed by decades of expertise. Whether you are filing complex corporate returns or need guidance on the nuances of small business taxes, discover how our essential guide to small business tax filing and personalized service can help. Don’t wait until deadlines or errors cost you more. Take the next step toward tax confidence today with APC1040.com.

Frequently Asked Questions

What is a corporate tax return?

Corporate tax returns are important financial documents that businesses use to report their income, expenses, and calculate their tax liabilities. They serve purposes like determining tax obligations, documenting financial performance, ensuring legal compliance, and providing transparency of corporate activities.

What types of business entities need to file corporate tax returns?

Various business entities must file corporate tax returns, including sole proprietorships, partnerships, corporations, S corporations, and limited liability companies (LLCs). Each has distinct filing requirements based on their structures.

What are the key filing deadlines for corporate tax returns?

Key filing deadlines vary by business type: Corporations must file Form 1120 by April 15, Partnerships must file Form 1065 by March 15, S Corporations file Form 1120S by March 15, and Sole Proprietorships submit Schedule C with their personal tax return by April 15.

What are some common mistakes to avoid when filing corporate tax returns?

Common mistakes include incorrect entity classification, underreporting income, misclassifying employees, inadequate record-keeping, and improperly claiming deductions. These errors can lead to audits, penalties, and legal complications.