How to Transfer IRA Money to Charity Without Paying Taxes

Giving to charity is one of the best ways to support causes you care about. But when it comes to making donations in retirement, many people wonder: Can I use my IRA to give money to charity without paying taxes? The answer is yes, thanks to a provision in the tax code called a Qualified Charitable Distribution (QCD). By understanding how this works, retirees can both fulfill their charitable goals and reduce taxable income at the same time.

This article will show you how to transfer IRA money to charity tax free, who qualifies, how much you can give and the exact steps to follow.

What is a Qualified Charitable Distribution (QCD)?

A Qualified Charitable Distribution is a direct transfer of funds from your Individual Retirement Account (IRA) to an eligible charity. Unlike normal withdrawals from a traditional IRA, a QCD is not included in taxable income.

In simple terms, it lets you:

- Donate money directly from your IRA to charity.

- Not pay ordinary income tax on the withdrawal.

- Count the donation towards your Required Minimum Distribution (RMD) if you’re 73 or older.

For many retirees, this strategy allows them to meet their RMD, support causes they care about and reduce their tax liability all at once.

How to Donate IRA Money to Charity

There are several ways to transfer IRA money to charity, each with different tax implications. You can choose the method that fits your age, financial situation and giving goals.

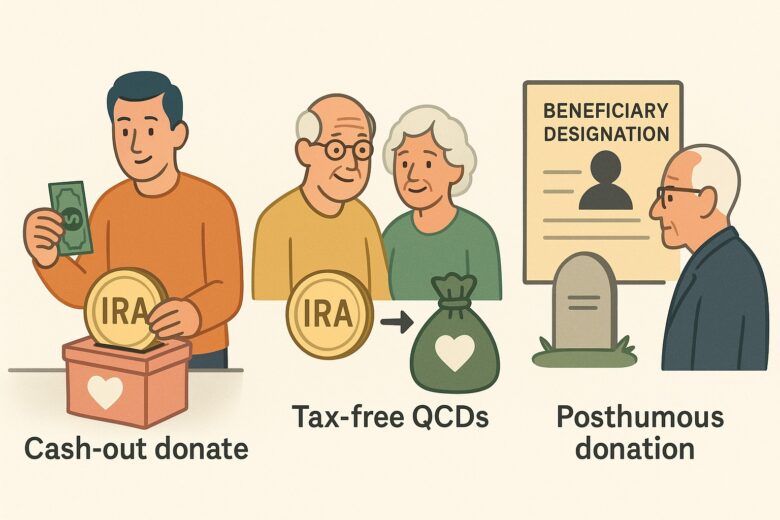

1) Cash-out and donate (with taxes)

One way is to withdraw funds from your IRA, pay income tax on the distribution and then donate the remaining amount to charity. While easy, this option is usually less tax efficient. The withdrawal adds to your taxable income and the charitable deduction only helps if you itemize instead of taking the standard deduction. This can be done at any age but usually provides little financial benefit.

2) Tax-free QCDs for those 70½ and older

For those 70½ and older, a more tax-efficient option is a QCD. This allows money to be transferred directly from your IRA to a qualified charity without being included in taxable income. You can give up to $108,000 per year individually or $216,000 as a couple and if you’re 73 or older, the amount also counts towards your Required Minimum Distribution. Since QCDs reduce your Adjusted Gross Income, they may lower your Medicare premiums and Social Security taxes and you don’t need to itemize deductions.

3) Posthumous donations via beneficiary designations

Another option is to name a charity as your IRA beneficiary, either for the full balance or just a portion. This ensures the charity gets the funds tax-free after your lifetime and also provides estate tax benefits. Since charities don’t pay income tax, they can use the entire inherited amount, unlike individual beneficiaries who would owe taxes on distributions. If preferred, you can designate a Donor-Advised Fund as the beneficiary to simplify administration while still supporting multiple charities.

How to Transfer IRA Money to Charity Without Paying Taxes

Transferring IRA funds to charity tax-free requires attention to rules and procedures. Qualified Charitable Distributions (QCDs) offer big tax benefits when done correctly. For a successful QCD follow these steps:

Step 1: Verify Eligibility

You must be at least 70½ years old at the time of the transfer for it to be considered a QCD. The transfer must come from a traditional IRA (some SEP and SIMPLE IRAs also qualify if inactive). The recipient must qualify as a 501(c)(3) public charity. The rules exclude donor-advised funds, private foundations, and supporting organizations.

Step 2: Choose Your Charity Carefully

Make sure your chosen organization is recognized by the IRS as tax-exempt. You can use the IRS Tax-Exempt Organization Search Tool online. A pro tip is to get a written acknowledgment from the charity confirming no goods or services were received in exchange for your gift.

Step 3: Contact Your IRA Custodian

The transfer must be made directly from your IRA to the charity, not through your personal account. Contact your IRA provider and request a QCD transfer. Most custodians have forms available online or can guide you through the process over the phone. Specify the exact dollar amount you want to transfer. Do not withdraw the funds yourself and then write a personal check, this will be considered taxable income.

Step 4: Keep Accurate Records

Your IRA custodian will issue a 1099-R form for the distribution, but it will not specifically identify it as a QCD. You must report it correctly on Form 1040 by excluding it from taxable income and writing “QCD” next to the line item.

Step 5: Plan for the Calendar Year

The transfer must clear by December 31 to count towards that year’s RMD or tax benefit. Start the process early to avoid year-end delays.

Eligibility Rules for IRA-to-Charity Transfers

The QCD strategy has strict IRS requirements you must meet before proceeding.

- Age Requirement: You must be at least 70½ years old on the date of the transfer.

- Account Type: Only traditional IRAs are eligible. 401(k)s, 403(b)s and other plans do not qualify unless rolled into an IRA.

- Charity Requirement: The recipient must be a qualified public charity (501(c)(3)). Private foundations, donor-advised funds and supporting organizations do not qualify.

- Direct Transfer Rule: The IRA custodian must send the funds directly to the charity. If the money passes through your hands, it becomes taxable income.

- Annual Cap: Up to $100,000 per year per person can be transferred tax-free. Married couples can each transfer $100,000.

Common QCD Mistakes

Even experienced donors make these errors:

- Taking the Money First: If the distribution is made to you and then donated, it becomes taxable income.

- Donating to Ineligible Organizations: Donor-advised funds and private foundations don’t qualify.

- Missing the Deadline: QCDs must be completed by December 31st for the tax year.

- Failing to Get Documentation: Without written acknowledgment, the IRS could disallow the tax benefit.

- Exceeding the Limit: Donations above $100,000 per year won’t be excluded from income.

Ready to get started now? Get expert help with QCDs and optimize your tax savings. Visit apc1040.com today to see what charitable giving strategies work best for you.

Strategies to Maximize Impact

Here are ways to get the most out of IRA-to-charity transfers:

- Bunch QCDs: Make larger QCDs in high-income years to offset taxable income.

- Coordinate with RMDs: Request your QCD early in the year to satisfy RMD first.

- Use Appreciated Assets for Other Giving: Donate stock from taxable accounts for extra tax benefits.

- Spousal QCDs: Each spouse with their own IRA can donate $100,000 per year, doubling the benefit.

- Name Charity as Beneficiary: Reduce estate taxes and leave pre-tax assets to charity.

Conclusion: Giving Smarter, Tax Smarter

Transferring IRA funds to charity through a QCD is one of the most tax-efficient ways to give. You can support your favorite causes, reduce taxable income and satisfy your RMD all in one move. Just follow the IRS rules, coordinate with your IRA custodian and keep good records.

If you’re thinking of this strategy, consult a CPA or tax advisor to ensure proper reporting and maximize the tax benefit. Apc1040.com can help you avoid costly mistakes and make the most of your retirement funds while giving back.