Did you know that over 22 million Americans report rental income on their taxes each year? Staying organized with your rental property records can mean the difference between a smooth tax season and unexpected problems. When every receipt, payment, and deduction has a place, you set yourself up for fewer headaches and potentially bigger savings at tax time. With some smart preparation, managing your rental taxes becomes much easier and more rewarding.

Step 1: Gather Essential Rental Income Records

Successfully tracking your rental income starts with meticulous record keeping. This step will help you organize all your financial documents so tax time becomes smooth and stress free.

Begin by collecting every financial document related to your rental property. According to IRS guidance, you need comprehensive documentation for all types of rental income. This means tracking not just standard monthly rent checks but also advance rent payments, security deposits you keep, lease cancellation fees, and even non-cash payments like services exchanged.

Create a dedicated folder or digital system where you can systematically store all income-related documents. Include items like:

• Rent receipts

• Bank statements showing rental deposits

• Lease agreements

• Forms 1099-K or 1099-MISC

• Canceled checks

• Electronic payment records

Digital tracking makes this process much easier. Consider using spreadsheet software or specialized accounting apps that allow you to categorize and timestamp each income transaction. This approach not only simplifies tax preparation but also provides a clear audit trail if the IRS ever requests documentation.

Pro Tip: Maintain records for at least three years after filing your tax return. The IRS recommends thorough documentation to support every item you report.

By establishing a consistent record-keeping system now, you’ll save yourself significant time and potential headaches during tax season. Check out our guide on income tax recordkeeping for more detailed strategies to manage your rental property finances like a pro.

Step 2: Organize Deductible Expenses and Documentation

Maximizing your rental property tax benefits starts with understanding and properly documenting your deductible expenses. This section will help you identify which costs can reduce your taxable rental income and how to track them effectively.

According to IRS Publication 527, rental property owners can deduct ordinary and necessary expenses that support property management. This includes a wide range of costs such as mortgage interest, property taxes, insurance, maintenance, utilities, and repair expenses. The key is knowing exactly what qualifies and maintaining precise documentation for each expense.

Start by creating separate categories for your rental property expenses. Group your costs into clear classifications like:

• Recurring operational expenses

• Maintenance and repair costs

• Property management fees

• Insurance and property tax payments

• Utility expenses

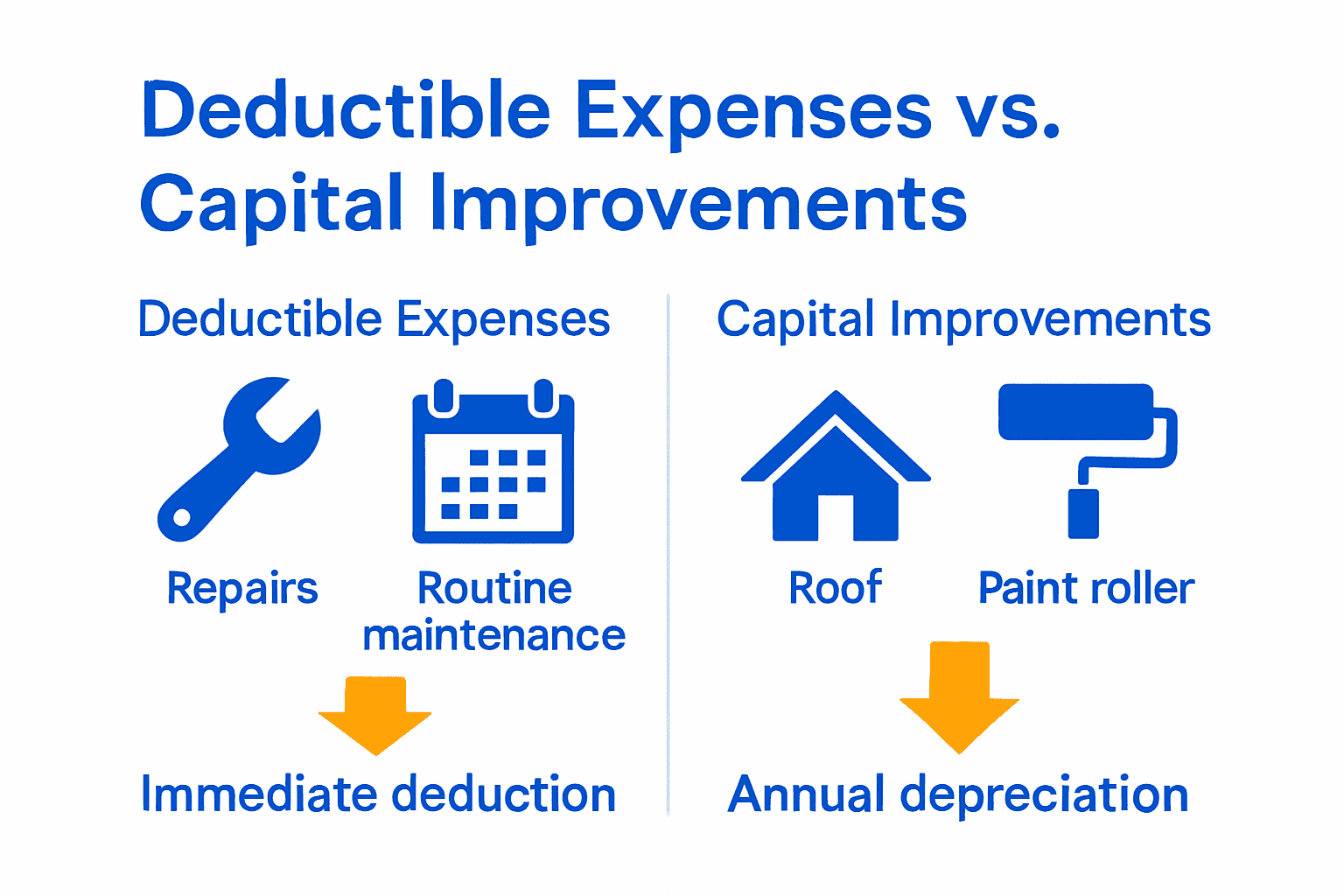

Important distinctions matter when tracking expenses. As the IRS explains, improvements must be capitalized and depreciated differently from standard repairs. For instance, replacing a roof is considered an improvement and needs to be depreciated over time, while fixing a leaky faucet counts as a standard repair you can deduct immediately.

Pro Tip: Always keep original receipts, invoices, and bank statements as proof of your expenses. Digital scans work perfectly for long term storage.

Professional tracking becomes simpler with modern accounting tools. Learn more about managing business deductions to streamline your rental property financial management. By establishing a robust documentation system now, you will save significant time during tax preparation and potentially maximize your allowable deductions.

Here’s a summary of common deductible expenses versus capital improvements:

| Expense Type | Deductible in Year Paid | Requires Depreciation |

|---|---|---|

| Repairs (leaky faucet) | Yes | No |

| Routine maintenance | Yes | No |

| Property management | Yes | No |

| Insurance premiums | Yes | No |

| Mortgage interest | Yes | No |

| New roof installation | No | Yes |

| Major renovations | No | Yes |

Step 3: Report Rental Income on Relevant Tax Forms

Reporting your rental income accurately is crucial for staying compliant with tax regulations and avoiding potential IRS audits. This step will guide you through selecting the right tax forms and documenting your rental property financials correctly.

According to IRS Topic No. 414, most residential rental properties use Schedule E on Form 1040. This form allows you to report income, deductible expenses, and depreciation for each rental property. If you own multiple properties, you might need to complete multiple Schedule E forms to capture all your rental income details.

The process requires careful attention to the specific nature of your rental activity. Standard residential rentals with no additional services will use Schedule E. However, if you provide substantial services like regular cleaning or maid service, you might need to report your income on Schedule C instead.

When completing Schedule E, you will need to include:

• Total rental income received

• Expenses like mortgage interest

• Property management costs

• Maintenance and repair expenditures

• Depreciation calculations

Depreciation gets calculated on Form 4562, which tracks the gradual reduction in property value over time. This can be a complex calculation, so consider consulting a tax professional if you are unsure about the specifics.

Pro Tip: Keep all supporting documentation. The IRS may request proof of the income and expenses you report.

Understand more about rental property taxes to ensure you are capturing every detail correctly. By mastering these reporting requirements, you will streamline your tax filing and maximize your potential deductions.

Step 4: Apply Eligible Deductions and Credits

Maximizing your tax savings as a rental property owner requires strategic understanding of available deductions and credits. This section will walk you through identifying and applying the most beneficial tax advantages for your rental income.

According to IRS Publication 527, rental property owners have several powerful depreciation strategies at their disposal. The Modified Accelerated Cost Recovery System (MACRS) allows you to recover your property’s cost through systematic annual deductions. This means you can gradually write off your property’s value over its useful life, potentially reducing your taxable income significantly.

One exciting opportunity for rental property investors is the Qualified Business Income (QBI) deduction. If your rental activity meets specific trade or business standards, you might qualify for an additional 20% deduction on your rental income. This can represent a substantial tax savings opportunity for property owners who actively manage their rentals.

Key deductions to consider include:

• Mortgage interest

• Property tax payments

• Operating expenses

• Maintenance and repair costs

• Travel expenses related to property management

Be aware of potential limitations. Passive activity loss rules and at risk regulations can restrict how much you can deduct in any given tax year. These complex rules determine whether your rental losses can offset other income or must be carried forward.

Pro Tip: Keep meticulous records of every expense. Documentation is your best defense during potential IRS reviews.

Learn more about maximizing your tax refund to ensure you are capturing every possible tax advantage. By understanding these deduction strategies, you can transform your rental property from a simple investment into a more tax efficihttps://apc1040.com/web-stories/tax-refund-hacks-simple-tricks-for-a-bigger-paydayent financial asset.

Step 5: Review and Submit Your Rental Tax Return

Finishing your rental income tax return requires careful review and attention to critical details. This final step ensures you submit an accurate and compliant tax document that maximizes your potential tax benefits.

According to the 2024 Instructions for Schedule E, multiple rental properties require special consideration during tax filing. You will need to carefully review each property’s financial details and determine whether additional supporting forms are necessary. The IRS specifically recommends attaching Forms 8582 or 6198 to document any potential losses from your rental activities.

Before submitting, conduct a comprehensive review of your documentation. Verify that all income sources are accurately reported and cross check your expense calculations. Pay special attention to depreciation figures, mortgage interest deductions, and any potential Qualified Business Income (QBI) deduction eligibility.

Key areas to double check include:

• Total rental income amounts

• Itemized expense calculations

• Depreciation figures

• Supporting documentation completeness

• Mathematical accuracy of all entries

If you own multiple properties or have complex rental arrangements, the reporting requirements can become intricate. Passive activity loss rules and at risk regulations might limit your deductible losses, so careful documentation becomes crucial.

Pro Tip: Consider a final review by a tax professional to catch any potential errors or missed deduction opportunities.

Learn more about submitting tax returns online to ensure a smooth filing process. By meticulously reviewing your rental tax return, you protect yourself from potential audits and optimize your tax outcome.

Unlock Stress-Free Rental Income Tax Filing in Akron

Tracking every rent payment, organizing deductible expenses, and navigating IRS forms can be overwhelming. If you are feeling lost on how to manage your rental property taxes or worry about missing eligible deductions and credits, you are not alone. Our guide showed how quickly paperwork builds up and how easily mistakes happen if you do not have expert support. You worked hard for your investment. Do not risk costly errors or missed opportunities at tax time.

Ready for absolute clarity and real savings on your rental property taxes? Now is the time to connect with local professionals who understand every step of the process. Let APC 1040 handle the details so you get maximum refund potential and total peace of mind.

Take the guesswork out of your next tax season. Visit our income tax recordkeeping guide or book your rental property tax review with our Akron specialists today. Secure your appointment soon as peak filing season books up fast.

Frequently Asked Questions

What expenses can I deduct when filing taxes on my rental property?

You can deduct various expenses such as mortgage interest, property management fees, repairs, and maintenance costs. Organize these expenses into categories and keep original receipts to ensure accurate reporting and maximization of your tax deductions.

What tax forms do I need to report my rental income accurately?

Most residential rental properties require you to report income using Schedule E on Form 1040. If you provide substantial services to your tenants, you may need to use Schedule C instead, so be sure to choose the form that accurately reflects your rental activity.

How can I maximize deductions and credits for my rental property?

Maximize your rental property deductions by understanding eligible expenses, including mortgage interest and depreciation. Keep thorough records of all expenses you incur, as this will support your claims and potentially reduce your taxable income significantly.

What should I double-check before submitting my rental tax return?

Before submitting your rental tax return, verify total rental income, itemized expenses, and depreciation calculations. Ensure all supporting documentation is complete to avoid issues during audits and to capture all possible deductions.

When is the best time to start organizing my rental income tax records?

Start organizing your rental income tax records as soon as you receive rental payments and incur expenses. This proactive approach will save you time and stress during tax season, allowing you to maintain a clear overview of your financial situation.